Kromer calls for analysis of the outcomes of tax collection sales

Specialist in the design and implementation of reinvestment strategies for metropolitan-area communities believes a land bank could generate substantial new funding for the maintenance of vacant properties, without necessitating major changes in how tax collection sales are currently conducted

September 29, 2013

TO: Council President Darrell L. Clarke, Councilwoman Maria D. Quiñones-Sanchez, Michael Koonce, Executive Vice President, PHDC, Brian Abernathy, Executive Director, PRA

FROM: John Kromer

SUBJECT: Proposal for a Game-Changing Use of Land Bank Powers

As a person who has worked with City of Philadelphia development agencies and City Council members to find creative ways to address the problem of blighted properties in Philadelphia neighborhoods, I’m very appreciative of the attention you have devoted to considering ways in which powers granted under the recently approved Pennsylvania land bank enabling legislation could be used to make Philadelphia’s response to this problem more effective.

However, I’m concerned that much of the current dialogue about the prospects for creating a Philadelphia land bank has focused on issues of secondary importance and overlooked an opportunity to use the legislation to fundamentally improve our anti-blight approach and establish a highly productive new model for returning neglected properties to the mainstream real estate market.

The Wrong Emphasis

In the current consideration of a proposed City Council Ordinance that would approve the establishment of a Philadelphia land bank, a disproportionately large amount of attention has been given to two issues, while not enough attention has been devoted to a third, much more important matter.

Conveyance of Surplus Properties. Some advocates for a Philadelphia land bank believe that the land bank should take ownership of all properties owned by city agencies and city-related authorities, thereby becoming a “one-stop shop” for interested developers that would manage property disposition in a systematic, reliable way. The problem with this approach is that most or all of the public-sector properties that would be available for transfer to a land bank are likely to have very low market potential. The most marketable properties that had been held in public-sector inventories are likely to have been sold years ago; and the size, condition, and/or location characteristics of most of the remaining properties are likely to make them poor prospects for sale, at least in the short term.

The city administration would not gain anything by transferring properties with low market potential to the land bank—it would just be transferring the problem to a new entity, which would then become a new target for criticism. Instead, the city administration’s policy should be to limit transfers of government-owned property to the land bank to 1) properties for which the land bank had identified and pre-qualified a developer or other recipient ready to accept immediate conveyance; 2) properties that appear to have good market potential in the short term (one to three years); and 3) properties for which property maintenance funding had been committed in advance to support asset management responsibilities associated with the land bank’s ownership of the property. Properties in each of these three categories could be identified on a quarterly basis, and any required departmental/agency actions needed to discharge governmental liens or encumbrances associated with them would take place immediately.

Councilmanic Perogative. Concerns have been voiced about whether individual land bank transactions should be subject to district Council member approval, and some supporters of a Philadelphia land bank have proposed that the so-called “Councilmanic prerogative” not be applied to land bank transactions. Based on my past experience in coordinating real estate transactions similar to those proposed to be undertaken by the land bank, I feel that this concern is unwarranted. District Council member approval of land bank transactions would be reasonable and constructive. Opponents of a District Council member signoff may be overlooking the fact that the land bank will not be managing the acquisition and disposition of major development sites; with relatively few exceptions, the land bank will be focusing on the task of finding appropriate developers and reuses for small and medium-sized properties that have attracted little or no interest in the private real estate market. I think it very likely that district Council members would welcome the opportunity to work with development agencies and land bank representatives to support the best outcomes for properties of this kind and would most often be prepared to support conveyance and reuse goals proposed by the city administration.

Property Maintenance Funding. At the same time, not enough attention has been devoted to the need to identify a dedicated source of funding to support the maintenance of any properties that would be acquired by the land bank. Because city agencies and the Pennsylvania Horticultural Society have compiled extensive data on vacant property maintenance expenses during the past two city administrations, realistic estimates of the cost of maintaining a vacant building or lot are readily available—and we know that this cost is substantial. The state enabling legislation gives land banks the power to issue bonds and provides for land banks to share (for a limited time, on a limited basis) in property tax-collection proceeds associated with properties that it acquires. But a land bank bond issue would not be likely to obtain needed city support (particularly in light of what is viewed by many as the less-than-satisfactory results of the bond-financed Neighborhood Transformation Initiative), and the amount of revenue that property tax collection proceeds could generate–at least during the land bank’s initial years of operation–would not be nearly enough to support a significant property maintenance capability.

Opportunity to Move to Scale

Many blighted properties are also financially distressed properties, and Philadelphia’s marketplace for financially-distressed property transactions is the tax collection sale administered by the Sheriff’s Office in coordination with the city’s Revenue and Law departments. The biggest opportunity to make a game-changing impact on Philadelphia’s blight crisis is for a land bank, working in coordination with the city administration and Sheriff’s Office, to re-orient the tax collection sale process in a way that would provide substantial new benefit to the public at large without changing the basic structure of the current tax collection sale process and without creating disadvantages for current participants in tax collection sales.

Problems with Philadelphia’s Tax Collection Sales

Tax collection sales in Philadelphia are never poorly attended. Participation by prospective bidders remains consistently high, for two reasons:

-

Philadelphia’s real estate market is trending upward. The most recent quarterly report on Philadelphia house price indices by Kevin Gillen of the Fels Institute shows positive housing price appreciation rates occurring in nearly every section of the city, with the highest appreciation rate in North Philadelphia (“Philadelphia House Price Appreciation Rates by Neighborhood” in Kevin C. Gillen, Philadelphia House Price Indices , Fels Institute of Government, July 15, 2013 at http://tinyurl.com/lphdmg6).

-

Tax collection sales provide an opportunity for bidders to purchase properties at prices that are substantially lower than their market value.

Although many properties are purchased at tax collection sales every year, a significant number of properties offered at these sales fail to attract any bids because they are poorly located, are in poor condition or are located in Philadelphia’s weakest real estate markets. These unwanted properties—some of which are not even processed for tax collection sale because no bids are anticipated–are likely to be significant contributors to blight; if the owners aren’t bothering to pay property taxes, it’s likely that they aren’t bothering to maintain them properly either.

Powers granted under the Pennsylvania land bank legislation can be used to address the following three problems associated with Philadelphia’s tax collection sales as they are currently administered.

-

The sales are not designed to convey properties to winning bidders who are fully committed to developing, improving, and/or maintaining them in a manner that is consistent with city policies and neighborhood reinvestment plans.

-

The most desirable properties listed for each sale are probably being sold for substantially less than their market value, unnecessarily limiting the financial benefit that Philadelphia could achieve through these transactions.

-

The least desirable properties remain unsold, and no public agency has sufficient resources to ensure that these neglected, tax-delinquent properties are maintained properly until a responsible owner or developer can be found.

Insights from Reading, PA

I recently researched tax collection sale outcomes associated with properties located in Reading, Pennsylvania, and I expect that a comparable analysis of Philadelphia tax sale outcomes would produce similar findings. The fact that tax sales in Reading are governed by the Real Estate Tax Sale Law (RETSL) while the Municipal Claim and Tax Lien Law (MCTL) governs tax sales in Philadelphia does not affect the validity of a comparison between these two cities.

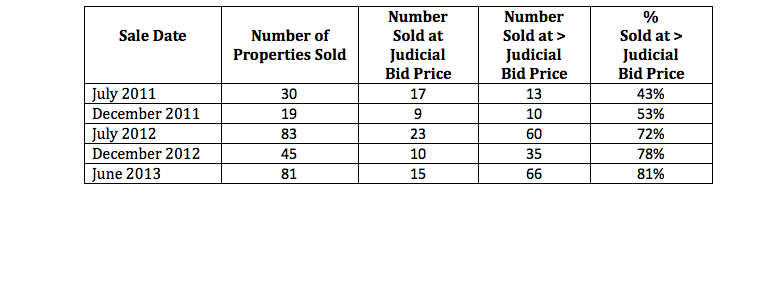

At the last five tax sales (the sales known as judicial sales or “free and clear” sales), held between 2011 and mid-2013, some properties located in Reading attracted prospective buyers who were willing to bid higher amounts than the judicial (minimum) bid price set by the county at the opening of the sale. The percentage of properties in this category increased at each of these five sales, from 43 percent in July 2011 to 81 percent in June 2013.

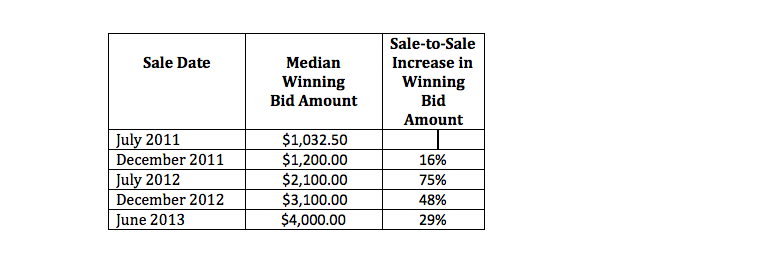

In these five sales, bidders were also willing to pay more in order to acquire the most desirable properties, as shown below. Between the July 2011 and June 2013 sales, the median winning bid amount quadrupled.

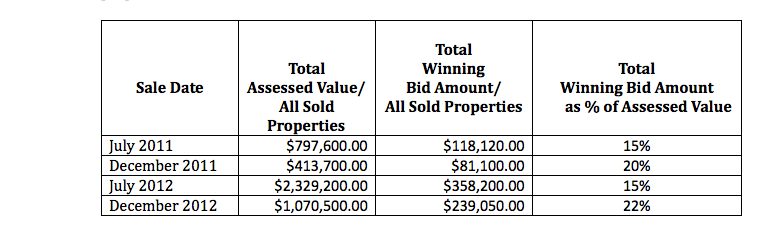

However, although median winning bid amounts increased in each of the five recent judicial sales, most of the properties were sold for substantially less than their assessed value. In four of these sales, the total winning bid amounts for properties that were sold represented one-fifth or less of the total assessed value of these properties.

At the same time, between a third and a half of properties located in Reading received no bids.

I expect that Philadelphia’s tax collection sale experience is similar to Reading’s. However, to my knowledge, a comparable analysis has not been completed for Philadelphia.

Using Land Bank Powers to Generate New Resources for Asset Management

The Pennsylvania land bank enabling legislation would make it possible for a Philadelphia land bank, based on an agreement with the city administration, to acquire properties listed for tax collection sale without having to bid against other participants in the sale. This power could be used constructively to generate a dedicated source of funding for the maintenance of properties in a land bank inventory.

A strategy for achieving this goal might be implemented in the following way.

- In preparing to list properties for a tax collection sale, the city administration and the Sheriff’s Office would perform all of the required due diligence (e.g., publication of advertisements and public notices, notification of lienholders) with no change in this process.

- All advertisements, notices, and related documentation would include a statement indicating that “The Philadelphia Land Bank may purchase one, some, or all of the properties listed for the tax collection sale” and that “Any properties purchased by the Philadelphia Land Bank are to be withdrawn from the sale.”

- On the day of the tax collection sale, based on a previously executed cooperation agreement between the land bank and the city administration, the land bank would purchase all properties listed for the sale.

- At the time advertised as the start of the tax sale auction, it would be announced that, although the Philadelphia Land Bank had purchased all of the properties listed for the tax collection sale (meaning that the tax collection sale would, in effect, be cancelled), an auction of most of the listed properties would take place immediately.

A list of properties to be auctioned would be distributed. The list would include all of the properties that had been previously advertised for the tax collection sale, with the following changes: a) properties that the land bank wanted to retain (for conveyance to a qualified developer or for inclusion in a site assemblage plan associated with a city policy or a neighborhood reinvestment plan) would not be included; and b) a surcharge in the amount of 10% of the winning bid would be imposed on all properties sold at the auction.

- The auction would be conducted in the same manner as the current tax collection auction is conducted. The auction would take place at the same location and would be managed by the same personnel. The only difference would be that the auction would be a land bank-sponsored auction rather than a Sheriff Sale.

-

The proceeds of the 10% surcharge would be used to capitalize a fund managed by the land bank that would be used exclusively to maintain properties for which no bids were received. These properties would be owned by the land bank until an appropriate developer and/or reuse is identified.

Feasibility of this Strategy

The feasibility of this approach could be assessed by reviewing records documenting the results of the past three years of tax collection sales. With data obtained from these records, it would be possible to consider the following, for each sale.

-

If a Philadelphia Land Bank had existed at the time of the sale, which of the listed properties would the land bank have retained and why? Which properties would have been conveyed to qualified developers? Which properties would have been acquired for inclusion in a site assemblage plan associated with a city policy or a neighborhood reinvestment plan?

-

If it is assumed (for the sake of argument) that the 10% surcharge would not discourage participation by bidders, how much funding would have been generated if the surcharge had been imposed on properties sold at these sales? I think that it is safe to make the above assumption because, even with the addition of a surcharge, winning bidders would continue to be able to obtain properties at bargain prices.

-

After the properties in items 1 and 2 above had been accounted for, what properties would the land bank be left with, what would it cost to maintain them, and how much of this expense could be covered by the surcharge proceeds?

The data needed in order to complete this analysis should be readily available, and the above and related questions could be evaluated by city agency staff and other interested parties in a short time. Independently of the city administration’s internal review, a team representing other parties participating in the current land bank dialogue could complete its own analysis and report on the conclusions they reached. Subject to the availability of data in a digitized format, a group of this kind could finish such an analysis and deliver a report within ten days. I would be glad to assist with related organizational and coordination tasks on a pro bono basis if that would be helpful.

Thank you for considering this proposal and my recommendations.

John Kromer

cc: Mayor Michael Nutter

WHYY is your source for fact-based, in-depth journalism and information. As a nonprofit organization, we rely on financial support from readers like you. Please give today.

Brought to you by PlanPhilly

PlanPhilly

In-depth, original reporting on housing, transportation, and development.

Judge denies PGW internal records of climate advocates, citing First Amendment protection

PGW sought emails, texts and memos from climate groups that are participating in its ratemaking case. The PUC ruled that would violate the First Amendment.

11 hours ago

Mayor Parker, unwavering in negotiations, dangles holiday pay incentive to end strike

Mayor Cherelle Parker is trying to end the DC33 union worker strike by Fourth of July with both the carrot and stick approaches. Here’s how.

22 hours ago

Philly residents, design experts bash latest proposal to replace Hoa Binh Plaza

OCF Realty is again trying to redevelop 1601 Washington Ave. as part of a broader movement away from the corridor’s industrial heritage.

1 day ago